config-i1

commented

2 years ago

config-i1

commented

2 years ago Looks like an issues with classes. Can you please provide a reproducible example (always do that if you can)?

Closed Steviey closed 2 years ago

config-i1

commented

2 years ago Looks like an issues with classes. Can you please provide a reproducible example (always do that if you can)?

Steviey

commented

2 years ago

Steviey

commented

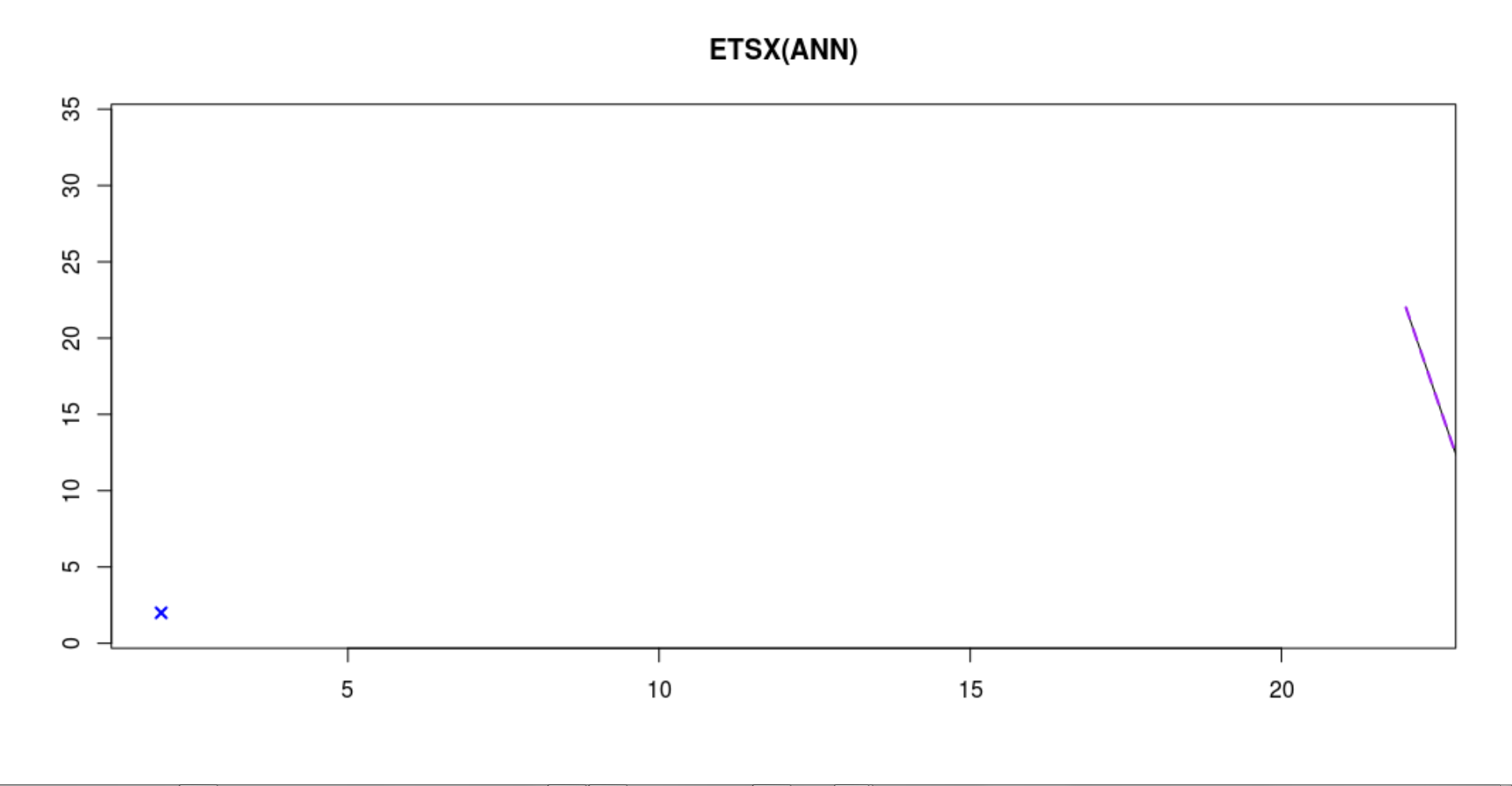

2 years ago The reproduce able example works fine so far. Now I have a difference between the example code and a 30K-line-script :-). Which let me think, it could be related to the data-source. What does the cross in the graph mean? Noticed 1: Even LASSO and RIDGE are working now -not in the 'live-code'...have to investigate... Noticed 2: Changing the model-def can lead to failure because of src (normal ETS-behaviour) Noticed 3: Setting cumulative=FALSE leads to 'Failed to return valid external regressors.' src-variance issue (normal) Noticed 4: Shuffling the data can lead to the initial issue (example code updated).

options(scipen = 999)

options(dplyr.summarise.inform=F)

options(max.print=2000)

library("Hmisc")

suppressPackageStartupMessages(library(lightgbm))

suppressPackageStartupMessages(library(digest))

suppressPackageStartupMessages(library(RSQLite))

suppressPackageStartupMessages(library(stringr))

suppressPackageStartupMessages(library(tidyr))

suppressPackageStartupMessages(library(dbplyr))

suppressPackageStartupMessages(library(rlang))

suppressPackageStartupMessages(library(freqdist))

suppressPackageStartupMessages(library(tidymodels))

options(tidymodels.dark = TRUE)

suppressPackageStartupMessages(library(modeltime))

suppressPackageStartupMessages(library(modeltime.ensemble))

suppressPackageStartupMessages(library(modeltime.resample))

suppressPackageStartupMessages(library(timetk))

suppressPackageStartupMessages(library(tidyverse))

suppressPackageStartupMessages(library(rsample))

suppressPackageStartupMessages(library(tidyquant))

suppressPackageStartupMessages(library(tibbletime))

suppressPackageStartupMessages(library(anomalize))

suppressPackageStartupMessages(library(smooth))

suppressPackageStartupMessages(library(lmtest))

suppressPackageStartupMessages(library(mgcv))

suppressPackageStartupMessages(library(fable))

suppressPackageStartupMessages(library(fabletools))

suppressPackageStartupMessages(library(tsibble))

suppressPackageStartupMessages(library(tsibbledata))

suppressPackageStartupMessages(library(tsfeatures))

suppressPackageStartupMessages(library(ggplot2))

suppressPackageStartupMessages(library(ggrepel))

suppressPackageStartupMessages(library(runner))

suppressPackageStartupMessages(library(ggformula))

suppressPackageStartupMessages(library(fANCOVA))

suppressPackageStartupMessages(library(stats))

suppressPackageStartupMessages(library(TTR))

suppressPackageStartupMessages(library(xts))

suppressPackageStartupMessages(library(vip))

suppressPackageStartupMessages(library(yardstick))

suppressPackageStartupMessages(library(plotly))

suppressPackageStartupMessages(library(catboost))

suppressPackageStartupMessages(library(treesnip))

suppressPackageStartupMessages(library(broom))

suppressPackageStartupMessages(library(finetune))

suppressPackageStartupMessages(library(tabnet))

prepModteltimeData<-function(df){

ret<-list()

rownames(df) <- NULL

df <- df %>% dplyr::mutate(id=row_number()) %>% relocate(id)

ret$df <- df

df_tsbl <- df %>%

as_tsibble(index=id)

df_split <- rsample::initial_time_split(df_tsbl, prop = 0.8)

train_len <- length(df_split$in_id)

test_len <- length(df_split$out_id)

df_tsbl <- as.data.frame(df_tsbl) # modeltime input format

splits <- df_tsbl %>%

timetk::time_series_split(assess=test_len, cumulative = TRUE)#kann auch int rein!

ret$df_train <- rsample::training(splits)

ret$df_test <- rsample::testing(splits)

ret$df_split<-df_split

ret$ts_split<-splits

myH<-1

myLimit <- as.numeric(nrow(df_tsbl)-myH)

ret$trainOneStep <- df %>% filter(id <= myLimit)

ret$testOneStep <- df %>% filter(id > myLimit)

return(ret)

}

getFormulaLocalEn<-function(xRegCols){

xRegCols <- xRegCols[xRegCols!='value']

xRegCols <- xRegCols[xRegCols!='id']

xRegCols <- xRegCols[xRegCols!='date']

myFormula <- xRegCols

myFormula <- paste0(myFormula, collapse= "+")

myFormula <- paste0('value ~ date + ',myFormula)

myFormula <- as.formula(myFormula)

return(myFormula)

}

y<-rnorm(120, mean=15, sd=5)

x<-c(

rep(0.08,20)

,rep(0.20,20)

,rep(0.40,20)

,rep(0.60,20)

,rep(0.80,20)

,rep(1.0,20)

)

x1<-c(

rep(0.18,20)

,rep(0.21,20)

,rep(0.10,20)

,rep(0.61,20)

,rep(0.81,20)

,rep(1.0,20)

)

data <-data.frame(value=y,xReg=x,xReg1=x1)

# shuffle (new)

rows <-sample(nrow(data))

data <-data[rows, ]

dataLength <-nrow(data)

myTime <-tk_make_timeseries("2011", length_out=dataLength, include_endpoints = FALSE)

data$date <-myTime

dataObj <-prepModteltimeData(data)

df_train <-dataObj$df_train

df_test <-dataObj$df_test

allData <-dplyr::bind_rows(df_train,df_test)

df_split <-rsample::initial_time_split(df_train, prop = 0.75)

train_len <-length(df_split$in_id)

test_len <-length(df_split$out_id)

myFormula <-getFormulaLocalEn(c('xReg','xReg1'))

recipe_spec <- recipe(myFormula,df_train)

set.seed(123)

cvResamples <- allData %>%

time_series_cv(

assess = test_len

,initial = train_len

,slice_limit = 10

)

lossVect = c("RIDGE","LASSO","GTMSE","likelihood","MSE","MAE","HAM","MSEh","TMSE","MSCE")

algoGrid <- expand.grid(

lossParam=lossVect

,dummy=c('A')

,stringsAsFactors = FALSE

,KEEP.OUT.ATTRS = FALSE

)

results <- vector(mode = 'numeric', length = nrow(algoGrid))

idx<-0

for(ee in seq_len(nrow(algoGrid))){

params <- algoGrid[ee, ]

myLoss <- as.character(params[1,'lossParam'])

print(myLoss)

model_spec <- adam_reg(

ets_model = 'ANN'

,loss = myLoss

,distribution = 'ds'

) %>%

set_engine("adam",silent=FALSE,h=1)

model_spec<-parsnip::eval_args(model_spec)

set.seed(123)

wflw<- workflow() %>%

add_model(model_spec) %>%

add_recipe(recipe_spec)

error<-tryCatch({

set.seed(123)

wflw_fit<-fit(wflw,df_train)

error<-0

}, warning = function(w) {

print(w)

return(0)

}, error = function(e) {

print(e)

return(1)

})

if(error>0){

msg<-paste('Loss-Function failed...',title)

}else{

print('kein Error')

}

}

infoTest <- cvResamples$splits[[1]] %>% analysis()

infoTest %>% glimpse()

infoTrain <- cvResamples$splits[[1]] %>% assessment()

infoTrain %>% glimpse()

myPlot<-cvResamples %>%

tk_time_series_cv_plan() %>%

plot_time_series_cv_plan(

date, value,

.facet_ncol = 1,

.interactive = TRUE

)

View(cvResamples)

View(infoTrain)

View(infoTest)

#print(myPlot)

stop('Finished!')

Shuffled except date-var:

Steviey

commented

2 years ago holdout seems to play a role...

model_spec <- exp_smoothing(

error = 'additive'

,trend = 'none'

,season = 'none'

# ,damping = 1

# ,smooth_level = 1

# ,smooth_trend = param6

# ,smooth_seasonal = param7

) %>%

set_engine("smooth_es",holdout=TRUE,silent=FALSE)

model_spec<-parsnip::eval_args(model_spec)smooth::es() (via modeltime wrapper) Noticed 5: msg: <simpleWarning: The exogenous variables contain NAs! This may lead to problems during estimation and in forecasting. Substituting them with 0.>

... is preventing the plotting in smooth (via modeltime)... code add...

colVect <- c('value','xReg')

data <- data %>% dplyr::mutate_at(all_of(colVect),as.numeric)

data <- data %>% dplyr::mutate(xReg=lag(xReg,n=1))

# comment this out to get the effect...

data <- data %>% dplyr::mutate_at(vars(matches("xReg")), ~tidyr::replace_na(.x,mean(.x,na.rm=T)))Update: msg-issue: Solved, must be an internal from modeltime/tidymodels, because plotting of extracted model works as expected. Even with NA-msg.

Plotting an extracted model via smooth:

wflw_fit<-fit(wflw,df_train)

myModel<-wflw_fit[['fit']][['fit']][['fit']][['models']][['model_1']]

myPlot<-plot(myModel,7)

print(myPlot)

stop()Doing the same (plotting extracted model) with ADAM brings:

Fehler in if (any(noVariability) && any(all.vars(formulaToUse) %in% names(noVariability))) { : Fehlender Wert, wo TRUE/FALSE nötig ist

myModel <- adam(df_train,"ANN", silent=FALSE,h=12, holdout=TRUE)

myPlot <- plot(myModel,7)

#myPlot<-ggplotly(myPlot)

print(myPlot)

stop()Can't reproduce it native.

Steviey

commented

2 years ago I can reproduce the chart-design (native) by setting h=1

idx=120

y<-rnorm(idx, mean=15, sd=5)

x<-cbind(

x1 = rnorm(idx, mean=15, sd=5)

,x2 = rnorm(idx, mean=15, sd=5)

)

fitXregs <- data.frame(x=x,y=y,stringsAsFactors=F)

fitXregs <- fitXregs %>% dplyr::relocate(y)

myModel <- adam(fitXregs,"ANN",silent=FALSE,h=1,holdout=TRUE)

I' m not sure if this is right- comparing to the book-chapter....

https://openforecast.org/adam/SES.html

Hinting with ggplot+plotly

idx=120

y<-rnorm(idx, mean=15, sd=5)

x<-cbind(

x1 = rnorm(idx, mean=15, sd=5)

,x2 = rnorm(idx, mean=15, sd=5)

)

fitXregs <- data.frame(x=x,y=y,stringsAsFactors=F)

fitXregs <- fitXregs %>% dplyr::relocate(y)

myModel <- adam(fitXregs,"ANN",silent=TRUE,h=10,holdout=FALSE)

#myModel <- smooth::es(df_train,model='ANN',h=1,holdout=TRUE,silent=TRUE)

y <-myModel[['data']][['y']]

myFitted <-myModel[['fitted']]

myResiduals <-myModel[['residuals']]

myFc <-myModel[['forecast']]

myFuture <- data.frame(forecast=myFc)

myData <- data.frame(actual=y,fitted=myFitted,residuals=myResiduals)

dataLen <- nrow(myData)

myData <- dplyr::bind_rows(myData,myFuture)

myData <- myData %>% dplyr::mutate(id=row_number()) %>% relocate(id)

myIntercept <- myData[dataLen,'id']

# wide to long

library(reshape2)

subToLong = myData[,c(1,2,3,5)]

myData = melt(subToLong, id=c("id"))

myPlot <- ggplot(myData)

myPlot <- myPlot + geom_line(aes(x=id, y=value, colour=variable))

myPlot <- myPlot + geom_vline(xintercept=myIntercept, linetype="dashed", color = "#FF6900",size = 0.5)

myPlot <- myPlot + scale_colour_manual(values=c("black","red","blue"))

myPlot <- ggplotly(myPlot)

print(myPlot)

Noticed 6: It also has a problem with: 'h=1'. Since modeltime had the same for a while, it seems to be a common problem in fc-plots. Anyway, this hint was fun :-).

Finally: fixing the hint... finding the lost one step forward fc (h=1, ~conditional mean)... :-).

[...]

dataLen1 <- nrow(myData)

hintPoint <- myData[dataLen1,c('id','value')]

myPlot <- ggplot(myData)

myPlot <- myPlot + geom_line(aes(x=id, y=value, colour=variable))

myPlot <- myPlot + geom_vline(xintercept=myIntercept, linetype="dashed", color = "#FF6900",size = 0.5)

myPlot <- myPlot + scale_colour_manual(values=c("black","red","blue"))

myPlot <- myPlot + ggtitle(title)

myPlot <- myPlot + geom_point(data=hintPoint,aes(x=id, y=value), colour="green",size=3)

myPlot <- ggplotly(myPlot)

print(myPlot)Are you using the most recent version of the smooth package? I cannot reproduce this. Here is what I get for the first part of your code:

Also please make sure that you use the latest version of the greybox package

Steviey

commented

2 years ago I noticed yesterday, that my local versions are way to old. I am working on multiple instances, sorry.

Steviey

commented

2 years ago Windows 7, greybox 1.0.5.41001, smooth 3.1.6.41004, R version 4.0.5 I get the following:

idx=120

y<-rnorm(idx, mean=15, sd=5)

x<-cbind(

x1 = rnorm(idx, mean=15, sd=5)

,x2 = rnorm(idx, mean=15, sd=5)

)

fitXregs <- data.frame(x=x,y=y,stringsAsFactors=F)

fitXregs <- fitXregs %>% dplyr::relocate(y)

myModel <- adam(fitXregs,"ANN",silent=FALSE,h=10,holdout=TRUE)

idx=120

y<-rnorm(idx, mean=15, sd=5)

x<-cbind(

x1 = rnorm(idx, mean=15, sd=5)

,x2 = rnorm(idx, mean=15, sd=5)

)

fitXregs <- data.frame(x=x,y=y,stringsAsFactors=F)

fitXregs <- fitXregs %>% dplyr::relocate(y)

myModel <- adam(fitXregs,"ANN",silent=FALSE,h=1,holdout=TRUE)

config-i1

commented

2 years ago The same code can be simplified to (for reproducibility purposes, so that I do not need to load tidyverse packages):

idx <- 120

x<-cbind(

y = rnorm(idx, mean=15, sd=5),

x1 = rnorm(idx, mean=15, sd=5),

x2 = rnorm(idx, mean=15, sd=5)

)

fitXregs <- as.data.frame(x, stringsAsFactors=F)

myModel <- adam(fitXregs,"ANN",silent=FALSE,h=10,holdout=TRUE)But this is what I get:

And this is with h=1:

So, I still cannot reproduce this.

config-i1

commented

2 years ago I assume that this can be closed now.

Steviey

commented

2 years ago Should be environment related.

Hello, I get different model-graphs with the same data and model-definitions in adam, auto_adam and smooth::es() when setting silent=FALSE. Is this normal, and what do the x-axes of the plots represent?

I also get this graph fitting ADAM, while cross validation for loss-function. What does the x on the left side mean?